This guide and accompanying debt collection letter template and other documents will help your business to avoid cash flow problems by explaining the steps that you can take to recover money owed without resorting to going to court. It includes various options for you to think about such as alternative dispute resolution or using a debt collection agency (and how to find a good one if you do). For a handy pack that includes all the documents you need to get your debt collection strategy off on the right foot, together with a detailed how-to guide explaining when and how to use each document, see our Debt collection toolkit. It includes debt collection letter templates that you can tailor to your business needs and guidance on how to escalate matters if you still don’t get paid, all the way up to sending formal statutory demands for the debt.

This guide and accompanying debt collection letter template and other documents will help your business to avoid cash flow problems by explaining the steps that you can take to recover money owed without resorting to going to court. It includes various options for you to think about such as alternative dispute resolution or using a debt collection agency (and how to find a good one if you do). For a handy pack that includes all the documents you need to get your debt collection strategy off on the right foot, together with a detailed how-to guide explaining when and how to use each document, see our Debt collection toolkit. It includes debt collection letter templates that you can tailor to your business needs and guidance on how to escalate matters if you still don’t get paid, all the way up to sending formal statutory demands for the debt.

Contents

- What is a debt collection letter?

- What is a debt recovery letter?

- What steps can I take to recover a late payment without going to court?

- I have chased and no payment has been made. What can I do next?

- Do I have to allow payment of a debt by instalments?

- Should I use a debt collection agency to recover a debt I am owed?

- What do debt collection agencies cost?

- How do I choose a reputable debt collection agency?

- Are there any risks for my business if I use a debt collection agency?

- When should I use a lawyer to recover a debt I am owed?

What is a debt collection letter?

It's a letter used to chase an unpaid debt. It's used to remind whoever owes you money that the deadline for payment has passed, and ensures you have a clear paper trail chasing payment. It might also be called a debt recovery letter or a letter chasing payment. Before you send a debt collection letter, it's a good idea to make initial contact with your debtor to find out why there's been a delay in payment. This could be done by phone call or email, but follow up any phone calls with an email or letter confirming what was said on the call. It's important to keep a written record of your correspondence where possible.

What is a debt recovery letter?

It's another term for a debt collection letter. It serves as a reminder to anyone who has failed to pay one of your invoices on time and sets out the details of the unpaid invoice, including the date on which payment was due and how much should be paid (including any interest payable if applicable). This is an important part of any cashflow management and debt collection strategy for your business. A debt recovery letter is the first step in a process of escalation when a payment becomes late, so it is designed to be straightforward and polite for those who have overlooked your invoice, simply forgotten to pay or whose internal accounting system is perhaps less organised than yours. Our debt collection toolkit contains three debt collection letters to escalate matters a step at a time.

What steps can I take to recover a late payment without going to court?

Once a payment becomes late, you should immediately take steps to chase your debtor. Sending out a sequence of escalating debt collection letters is a great way to do this.

Note, if payment is delayed due to the COVID-19 pandemic, the Government has recommended that businesses adopt a fair and reasonable approach to chasing payments and avoiding adversarial disputes if at all possible. Although this is not legally binding, from a reputational standpoint and with future business in mind, you may decide to allow longer timescales or waive interest and late payment charges for customers or suppliers in difficulty, but this is entirely at your discretion.

The steps you take to chase payment of an invoice are ultimately a commercial decision for your business, but the below is a suggested cost-effective course of action to take before considering taking your debtor to court. These steps are supported by a how-to guide and all the relevant documents you need in our Debt collection toolkit.

- Make immediate contact

Find out why there has been a delay. Be polite and professional but make it clear that you expect payment within a certain time frame, and follow up with a further phone call or email if a specific time frame is agreed and payment is still not received. Follow up any phone calls with an email or letter confirming what was said. It is important to have a written record of your correspondence where possible. - Send debt collection letters

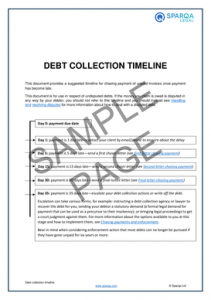

The below is a suggested timeline for escalation:- if your invoice remains unpaid five days after it has become late, send First debt collection letter;

- if your invoice remains unpaid 15 days after it has become late, send Second debt collection letter, explaining that if payment is not received promptly, you may charge interest on the debt and/or apply a late payment charge; and

- if your invoice remains unpaid 30 days after it has become late, send Final debt collection letter, explaining that if payment is not received, you will apply interest and other debt recovery charges (if appropriate) and will take further debt recovery action.

- Formally escalate your debt recovery actions

Consider the impact of taking formal action against a customer on your ongoing business relationship with them, and any cost implications of that. Weigh up whether the costs and time involved in escalating your debt recovery actions are worth your while or whether you would be better placed to simply write off the debt.See below for your main options and for a suggested timeline for chasing payment of unpaid invoices, see Debt collection timeline.

I have chased and no payment has been made. What can I do next?

If you have chased money owed to you by sending out a debt collection letter and following it up, there are various options available to you to press further. Consider whether any of the following are suitable:

- Using a debt collection agency or lawyer

This can be a cost-effective method of getting your money back if your relationship with your client has already broken down—see below for more information about when and how to do this. - Alternative dispute resolution (ADR)

You can use any alternative dispute resolution scheme that you are part of, for example if you are a member of a trade association which runs its own scheme. If the money is owed to you by a larger business, you might be able to complain to the Small Business Commissioner about them. The Government is encouraging businesses to use ADR during the COVID-19 pandemic, to help preserve business relationships and supply chains, and to avoid businesses embarking on adversarial legal disputes and/or making legal threats against one another. - Statutory demand

Consider sending your debtor a type of formal demand for payment, called a statutory demand. Note, however, the Government has temporarily changed the law to void statutory demands sent to companies between 1 March 2020 and 30 September 2021, to help businesses navigate the disruption caused by COVID-19. This means that any statutory demands sent during that time period cannot be used to try to wind up a company if it does not pay up. Individuals (including sole-traders, freelancers and the self-employed) are not covered by the new law, so the normal rules will continue apply to any statutory demands issued against them. - Selling the debt

You could sell the debt to someone else if you have immediate cash flow concerns and do not want to pursue the debt yourself. For example if you do not have the time or resources to do so – see below for more information about this. Such sales are usually at a substantial discount.

Do I have to allow payment of a debt by instalments?

In light of the disruption caused by the COVID-19 pandemic, the Government strongly recommends that you at least consider measures such as accepting payment of debts by instalments. However, unless your contract says that you must, it is your choice as to whether to accept a proposal for payment by instalments.

Accepting instalments necessarily involves you waiving your strict rights under your contract, so consider any such action carefully before you take it as you may be unable to go back on it if receiving payments by instalment becomes inconvenient later. It is sensible to agree any instalments clearly in writing, specifying that the arrangement is a one-off and that the usual contractual payment terms will apply for any and all other debts.

Should I use a debt collection agency to recover a debt I am owed?

Instructing a debt collection agency to recover a debt you are owed sends a strong message and if your business relationship has already disintegrated, it can be a cost-effective method of recovering some of the money you are owed in comparison to going to court. Due to the disruption caused by the COVID-19 pandemic, you may want to think more carefully than usual before taking any debt collection measures against distressed businesses or individuals which may be perceived as overly aggressive or unreasonable.

A debt collection agency will take over recovery of your unpaid invoice, investigating your debtor’s financial status, future trading prospects and ability to repay the debt. Usually they will either contact your debtor to organise a repayment plan or determine that your debtor will be unable to pay and recommend that you write off the debt rather than incurring the costs of pursuing them further.

Things to bear in mind when considering instructing a debt collection agency include:

- cost;

- reputational and legal risk; and

- there is a limit to what debt collection agencies can do. Debt collectors do not have the same powers as court bailiffs (which you can use once you have obtained a court judgment for the money owed) for example they cannot seize goods, or enter premises without being invited.

Remember that when you are giving your clients’ or customers’ financial information to a third party, you need to ensure that you comply with your data protection obligations. See The rules about sharing personal data for full details.

What do debt collection agencies cost?

Debt collection agencies charge a fee, which will usually be a percentage of the total amount of the debt and may also include a fixed administration fee. The percentage fee charged will likely be much larger if the payment is more than 90 days late, although many collection agencies also offer a ‘no collection no fee’ service, which reduces the cost risk to you of pursuing this option.

How do I choose a reputable debt collection agency?

Reputation is important. When instructing a debt collection agency, check their reputation eg using online searches or recommendations and ensure that you give clear instructions about what you do and do not expect them to do. It is also best practice for you or the debt collecting agency to contact your debtor to let them know who will now be making contact with them about their debt.

Choosing a reputable debt collection agency will minimise the risks of the agency (and by extension your business) breaking the law by distressing or harassing any debtors.

Are there any risks for my business if I use a debt collection agency?

Yes, if the agency is not a reputable one. It is an offence for debt collectors to harass debtors in a way which is meant to distress or humiliate them or members of their family or household. You could also be guilty of an offence and fined up to £5,000 if you are involved in the debt collector taking any such action (even if you do not act unlawfully yourself).

From a reputational standpoint, in light of the disruption caused by the COVID-19 pandemic you may want to think more carefully before taking any debt collection measures which may be seen as aggressive or unreasonable. The Government has issued guidance strongly recommending that businesses avoid taking steps which are likely to damage relationships and/or lead to disputes. Although this guidance is not legally binding, it is best practice to ensure you have considered all reasonable alternatives before using an agency to collect debts, and to ensure you choose a reputable one.

When should I use a lawyer to recover a debt I am owed?

As a result of the COVID-19 pandemic, you may want to think more carefully than usual before instructing a lawyer to pursue a debt. The Government is strongly encouraging businesses to find fair and reasonable solutions to payment disputes without resorting to lawyers. However this guidance is not legally binding, and particularly for larger overdue payments, hiring a solicitor is an option.

It may be appropriate for you to instruct a solicitor (rather than, say, a debt collection agent) if:

- your debtor is a larger business with good cash flow, or an individual who has means but is simply not paying up; and

- you are considering bringing legal action as a next step (this may depend on the value of the debt and you should bear in mind that it is possible to bring a small claim to court without the assistance of a lawyer – see Starting a small claim against someone else for guidance on doing this, including how to write your own letter before action using our templates (Letter before action, debt claims (B2B) if your debtor is another business and Letter before action, debt claims (B2C) if your debtor is a consumer)).

If your client or customer is experiencing financial difficulties, it is less likely that a strongly worded letter from a solicitor will elicit payment, and you should consider other debt recovery actions, such as sending them a statutory demand or bringing legal proceedings to allow you to enforce the debt in other ways, eg through taking security over your debtor’s property. In any event, it would be best practice to ensure you have considered all reasonable alternatives before instructing a solicitor.

Remember that when you are giving your clients’ or customers’ financial information to a third party, you need to ensure that you comply with your data protection obligations. See The rules about sharing personal data for full details.

The content in this article is up to date at the date of publishing. The information provided is intended only for information purposes, and is not for the purpose of providing legal advice. Sparqa Legal’s Terms of Use apply.

Helen Turnbull is Head of Strategic Development for the Marketplace at FromCounsel, the specialist corporate legal resource trusted by top global law firms and FTSE 100 companies. Before joining FromCounsel in 2021, Helen was Head of Content at Sparqa Legal. Having previously spent 12 years practising as a commercial and property law barrister, Helen regularly contributes her expertise to Sparqa’s blog.